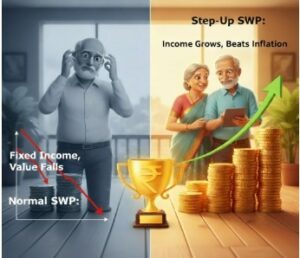

Balancing Risk and Return for Retirement💰✨

Retirement should be a time of peace, not financial worry. But that peace depends on the choices you make today. For many, the go-to retirement option is a Fixed Deposit (FD). While FDs provide safety, the real question is — are they enough to secure your future in an inflation-driven world?

🔎 The Problem with Fixed Deposits

FDs are popular for their guaranteed returns and capital protection. But they come with major limitations:

- Inflation Risk: If inflation averages 6% and your FD gives 6.5%, your “real return” is almost negligible.

- Low Liquidity: Premature withdrawal attracts penalties, reducing your returns. In many cases, such as a 5-year FD – non-breakable, you cannot access your money at all before maturity.

- Tax Burden: FD interest is fully taxable as per your income slab, further eating into your earnings.However, a 5-year FD qualifies for tax benefit under Section 80C (old regime only), though the interest earned is still taxable.

👉 Example: ₹10 lakh in an FD at 6.5% grows to ~₹17.5 lakh in 10 years. But with 6% inflation, its purchasing power is equal to only ~₹9.8 lakh in today’s money!

📈 Why Mutual Funds Can Be Smarter

Mutual Funds aim to deliver inflation-beating returns while giving you flexibility. They spread your money across equities, debt, or both — reducing risk through diversification.

- For Safety Seekers: Debt funds like Overnight, Liquid, or Short-Duration funds.

- For Growth Seekers: Equity funds with long-term compounding power based on their risk profile.

- For Retirement Income: Systematic Withdrawal Plan (SWP) creates a steady income stream, often more tax-efficient than FD interest.

👉 Example: ₹10 lakh invested in a Balanced Advantage Fund (assuming 10% CAGR) grows to ~₹26 lakh in 10 years — far better inflation-adjusted wealth.

🏦 Other Retirement-Safe Options

Along with Mutual Funds, you may consider:

Senior Citizen Savings Scheme (SCSS): ~8.2% guaranteed return.

Post Office Monthly Income Scheme (POMIS): Regular monthly interest payouts.

RBI Floating Rate Bonds: Safer, government-backed with variable rates.

Annuities / Pension Plans: Steady income, though with less flexibility.

🎯 Final Takeaway

FDs are safe but not sufficient for long-term wealth. A smart retirement portfolio blends:

✅ FDs for safety

✅ SCSS / RBI Bonds for stability

✅ Mutual Funds for growth + SWP for monthly income

The goal is not just to save, but to grow and protect the value of your money against inflation. With the right mix, your golden years can truly be golden. 🌟

👉To know more about this watch this video

👉 Speak to Dr. A.V. Senthil, Certified Financial Planner to create a retirement-ready investment mix tailored for your needs. The earlier you start, the stronger your financial independence will be.