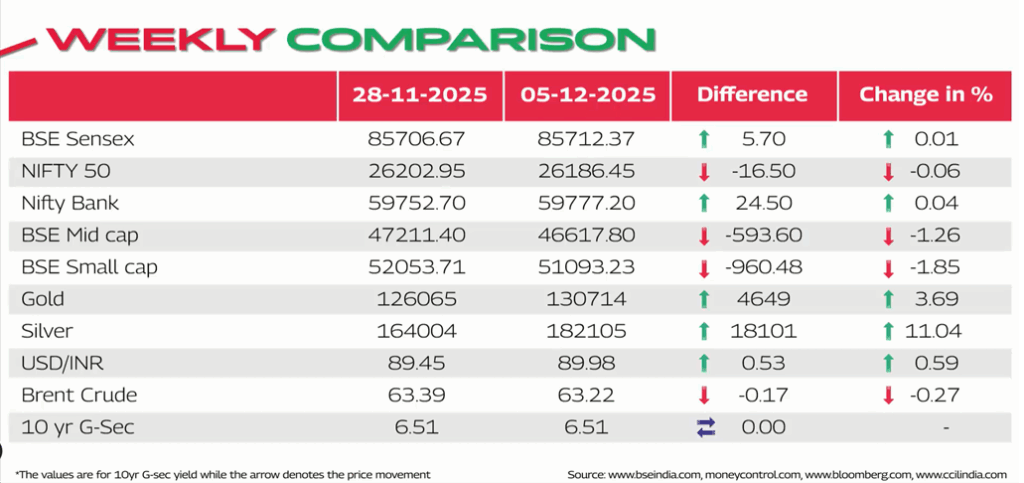

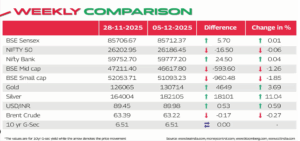

The Indian equity market witnessed a cautious trading week between 28th November and 5th December 2025. Bulls and bears continued their ongoing battle, resulting in muted index-level performance while volatility remained stock- and sector-specific.

📈 How Did the Markets Perform?

The large-cap indices remained steady, but midcap and smallcap segments faced notable pressure.

| Index | 28 Nov ’25 | 5 Dec ’25 | % Change |

| NIFTY | 26,203 | 26,186 | -0.1% |

| SENSEX | 85,707 | 85,712 | 0.0% |

| NSE500 | 23,933 | 23,835 | -0.4% |

| MIDCAP 100 | 61,043 | 60,595 | -0.7% |

| SMALLCAP 100 | 17,829 | 17,508 | -1.8% |

This highlights a risk-off approach as investors took money off broader market winners.

🚀 Top Gainers & Losers — Nifty 50

⬆️ Top Gainers

IT led the charge, supported by global tech optimism.

- Wipro Ltd.: +4.2%

- HCL Technologies: +3.6%

- Infosys Ltd.: +3.6%

- Tech Mahindra: +3.5%

- Asian Paints Ltd.: +3.3%

⬇️ Top Losers

Aviation, healthcare, and consumer names saw profit booking.

- InterGlobe Aviation Ltd.: -9.0%

- Max Healthcare: -5.6%

- Hindustan Unilever: -2.9%

- Eternal Ltd.: -2.6%

- Titan Company Ltd.: -2.4%

🔍 Nifty 500 — High Action Zone

⬆️ Biggest Gainers

- Birlasoft Ltd.: 13.8%

- Hindustan Copper Ltd.: 13.7%

- ZF Commercial Vehicle Systems: 12.0%

- Wockhardt Ltd.: 10.1%

- Onesource Specialty Pharma: 10.0%

⬇️ Biggest Losers

- Kaynes Technology: -20.7%

- Ola Electric Mobility: -13.6%

- Transformers & Rectifiers: -12.5%

- Hitachi Energy India: -12.5%

- Garden Reach Shipbuilders: -11.5%

A volatile week for broader market leaders with sharp swings in technology, energy, and defence plays.

▶️ Sector Snapshot — Weekly Change

✅ Top Performing Sectors

- IT: +3.5% (Strong Outperformer)

- Auto: +0.6%

- Metal: +0.5%

- Private Banks: +0.3%

✅ Weak Sectors

- Media: -2.3%

- PSU Banks: -1.6%

- Healthcare: -1.2%

- Realty: -1.1%

- Oil & Gas: -1.1%

✅ blueKey Market Drivers This Week

❇️ Major Macro Announcements:

- RBI Repo Rate Cut: Cut by 25 bps → 5.25%.

- Policy Stance: Changed to Neutral.

- GDP Forecast: FY26 growth forecast raised to 7.3% (earlier 6.8%).

- Liquidity Injection: RBI to inject liquidity via ₹1 lakh crore OMO bond purchases and a $5 billion USD/INR swap.

- IIP Growth: Stood at 0.4% in Oct’25 (modest).

- GST Collection: Eased to ₹1.7 lakh crore, a 1-year low.

These indicate a policy push for growth, but underlying consumption remains muted.

🔔 Events to Watch Next Week

- Sunday: Japan Q3 GDP numbers

- Tuesday: US JOLTs Job Openings

- Wednesday: US Core CPI

- Wednesday: US Fed Interest Rate Decision

- Friday: India CPI data

Central bank cues and inflation readings may add volatility to global and domestic markets.

🏁 Bottom Line

- Markets paused after months of strong gains.

- IT outperformed, while broader markets corrected.

- RBI’s measures support liquidity and growth.

- Upcoming inflation data will be key to near-term direction.

Stay tuned — volatility may continue as global and domestic triggers unfold.

FAQs

Q1. Why did smallcaps fall more than largecaps this week?

Investors locked in profits from recent outperformers, leading to a sharper correction in broader markets.

Q2. Which sector performed the best?

The IT sector, gaining +3.5% driven by renewed interest in tech majors.

Q3. Which was the biggest gaining stock?

Birlasoft, up 13.8% within the Nifty 500 universe.

Q4. What major policy change happened this week?

RBI cut the repo rate to 5.25% and shifted its stance to Neutral.

Source: JM Mutual Fund, Mahindra Mutual Fund

Disclaimer: Mutual fund investments are subject to market risks. Please read all scheme-related documents carefully before investing.

2 thoughts on “WRU13 – Weekly Market Pulse”

Useful consolidation of performance

Will be good compare side-by-side 3M, 6M and 12M performance for all.above stocks.

Sure, thanks for your valuable feedback.